Trends and investment in the SAP community 2026

The DSAG Investment Report 2026 reveals a picture characterized by scepticism: although general IT budgets continue to rise, investments in SAP software are being made in a much more targeted, selective and critical manner than in the past. The loyal user base is increasingly resisting the dictated cloud constraints. As a result, S/4 in on-prem operation remains a preferred choice for many companies, while the aggressively marketed pure cloud models are struggling to gain momentum.

For a worrying 70 percent of the companies surveyed, the restrictive and complex SAP license and contract structure is one of the biggest hurdles. For the critical SAP user, the conclusion is that although SAP remains strategically relevant as a transactional centerpiece, trust in the Walldorf pricing policy (SAP PKL) and cloud strategy has been permanently eroded. „The development of budgets reflects the ongoing economic pressure that many companies are under. Energy prices, geopolitical uncertainties and a tense market environment mean that investments are being scrutinized more critically and in some cases postponed - including in the SAP environment,“ says DSAG CEO Jens Hungershausen. From DSAG's point of view, companies are investing in a more targeted manner without fundamentally questioning SAP.

SAP cloud without exit

The path to the SAP cloud is sold to existing customers as the ultimate liberation and a haven of limitless agility, but an investigative look at the exit options reveals an unprecedented strategic abyss. The bitter truth, which is systematically concealed in the glossy brochures, is that SAP does not actually have a viable and standardized cloud exit strategy. Anyone who, as an existing SAP customer, embarks on the much-vaunted Rise with SAP model is entering a dangerous one-way street that is quite rightly referred to in specialist circles as a mathematical „trapdoor function“ - a path that is temptingly easy to enter, but from which there is virtually no technical or contractual escape.

„The results clearly show that companies no longer view SAP investments in isolation. Digital transformation and process modernization remain the key drivers, but are clearly flanked by the need to operate more efficiently and reliably meet regulatory and security requirements,“ says Jens Hungershausen. „Against a backdrop of economic uncertainty, rising costs and complex license and maintenance models, SAP investments must be innovative, economically viable and resilient at the same time.“

Complex license transformation

The risk of leaving the SAP cloud lies in the complex mechanics of license transformation, the so-called FUE gospel (Full Use Equivalent). In order to switch to the cloud, SAP forces customers to irrevocably give up the perpetual on-prem licenses (CapEx) they have purchased at great expense over decades and convert them to a pure rental model (OpEx) in the form of cloud subscriptions via a contract conversion. If the company terminates this contract or unforeseen economic hardship forces it to exit, the right to use the ERP software evaporates immediately.

Sovereignty over data scrap

The customer is then legally and technically barred from returning to their own on-prem world, as they have had to hand over the essential licenses at the cloud's pearly gates and it is impossible to reactivate the old ECC system. Another existential risk becomes apparent when looking at data sovereignty. Although SAP theoretically allows users to download their own data when leaving the cloud, this is a smokescreen. Naked table data and raw data exports are completely worthless without the business logic, i.e. without the proprietary SAP algorithms and the business context, and resemble a pile of data scrap.

In addition, there is an aggressive contractual component that DSAG lawyers have uncovered: SAP reserves the right in the cloud T&Cs to irrevocably delete customer data stored in the cloud just one day after the end of the contract. This forces companies under massive time and financial pressure to develop complex data retention strategies and set up expensive archiving systems in order to be able to comply with legal retention periods in the event of an exit.

The situation becomes particularly toxic if the cloud project is not even successfully completed and the target system never goes live. A Rise contract is a coupled construct consisting of a relocation service (lift and shift) and the cloud rental (subscription).

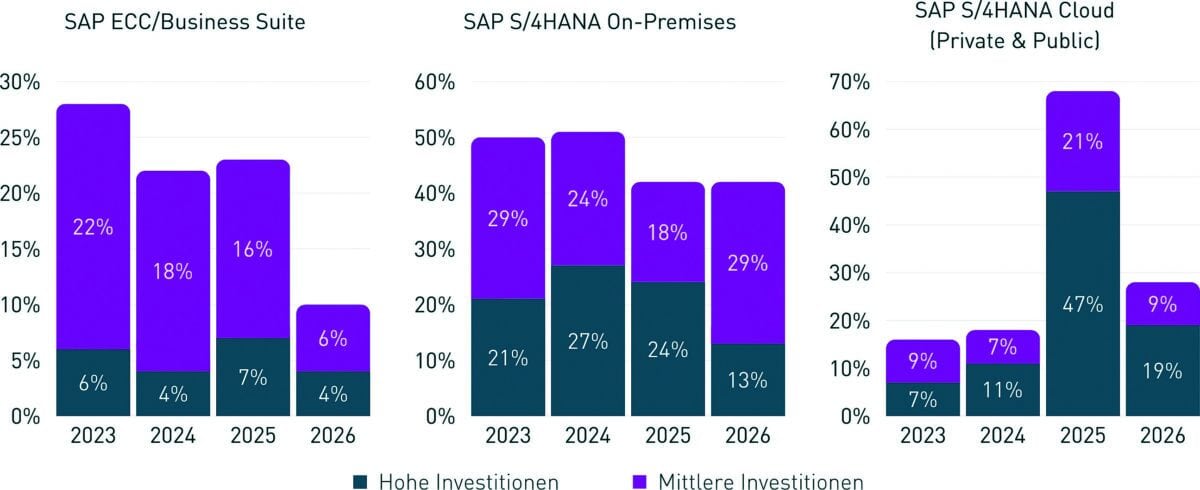

2023: n=265, 2024: n=228, 2025: n=243, 2026: n=198

If the complex migration fails due to historically grown data structures or the implementation partner's lack of experience, SAP still insists relentlessly on the ongoing payments for the cloud subscription. The customer is then left in an absolute no-man's land: they cannot go back to the on-prem world because the licenses have already been surrendered under the contract, and they cannot go forward to the cloud because the implementation has failed. In the worst case scenario, the SAP user has to pay rent for years for an „empty apartment“ in the cloud. Many long-suffering CIOs are currently pinning their hopes on the new EU Data Act, which is intended to break the lock-in effect, abolish switching fees and make it easier by law to switch cloud providers. However, the technical

The reality lags miles behind the legal ambitions from Brussels. Although the Data Act forces providers to hand over data and reduce technical hurdles through interoperability, it in no way solves the fundamental problem of missing application logic and expropriated software licenses after the end of a contract. As long as SAP remains silent about specific exit modalities and does not offer any fair exit clauses, the cloud exit remains a business game of vabanque.

AI between appearance and reality

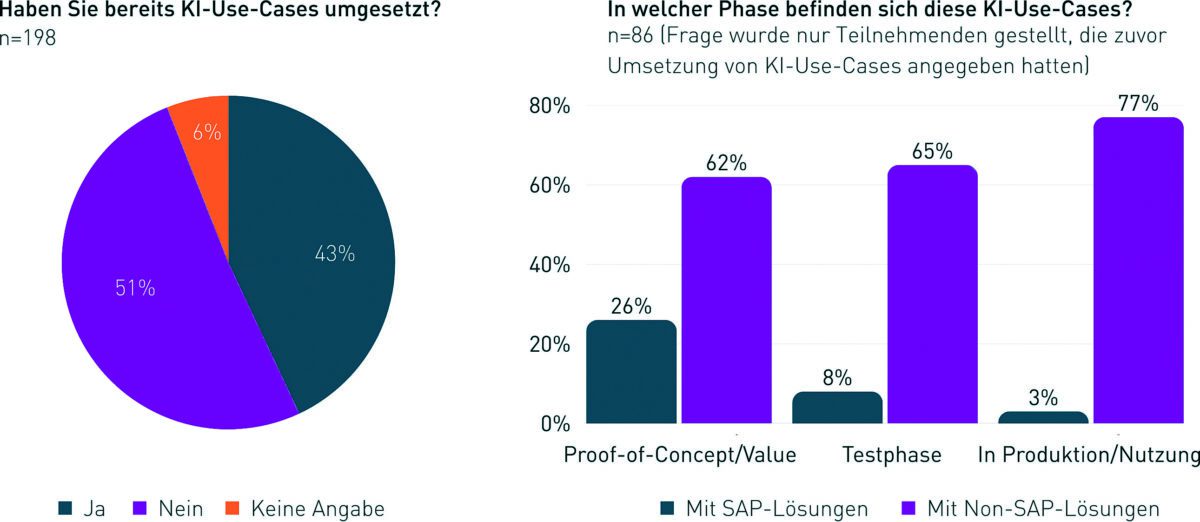

Another key technical and process-related topic for 2026 is the transition of artificial intelligence from the purely experimental phase to productive operations, with autonomous AI agents (agentic AI) set to become the new standard for digital workflows. SAP is promoting the AI assistant Joule and Business AI as revolutionary saviors, but the figures from the community drastically punish this marketing offensive. When DSAG members use artificial intelligence productively in use cases in 2026, 77 percent will use non-SAP solutions, while only a marginal three percent of companies will rely on SAP's original AI tools. This revelation clearly shows that user companies want to avoid the dreaded vendor lock-in in expensive cloud premium contracts and preserve their digital sovereignty by using external large language models (LLMs) and independent platforms.

After the S/4 migration boom

Very clear and cautionary words can also be heard from SAP partners in 2026, calling for a strategic realignment in consulting. Analysts from PAC in Munich and leading integrators are warning that the S/4 migration boom will soon peak, as more than half of companies will have completed the changeover by 2026. Purely technical conversion projects will no longer be enough to serve the market in the future, which is why SAP service providers will have to transform themselves from mere implementers to strategic consultants who deliver real business value through process optimization and AI-driven innovations.

For existing SAP customers, the year 2026 will see the crystallization of fundamental changes that go far beyond a simple software upgrade. The age of the monolithic ERP system, in which SAP reigned as the undisputed autocrat over data and processes, is coming to an irrevocable end and will be replaced by the vision of a modular composable ERP. In this new paradigm, companies orchestrate their business processes via an open multi-vendor architecture in which the Business Technology Platform (SAP BTP) occupies the top spot for strategic SaaS investments with 39 percent, but is necessarily combined with generic IT platforms and best-of-breed solutions from hyperscalers and third-party manufacturers.

Digital resilience and clean core

The much-publicized dictate of the clean core is also forcing users to banish their historical, often competition-differentiating Abap modifications from the system core and outsource them to platforms. True digital resilience today requires companies to have the entrepreneurial courage to take architectural sovereignty back into their own hands, to think in terms of hybrid structures and to stop being blindly driven by the sales-driven cloud narratives from Walldorf.

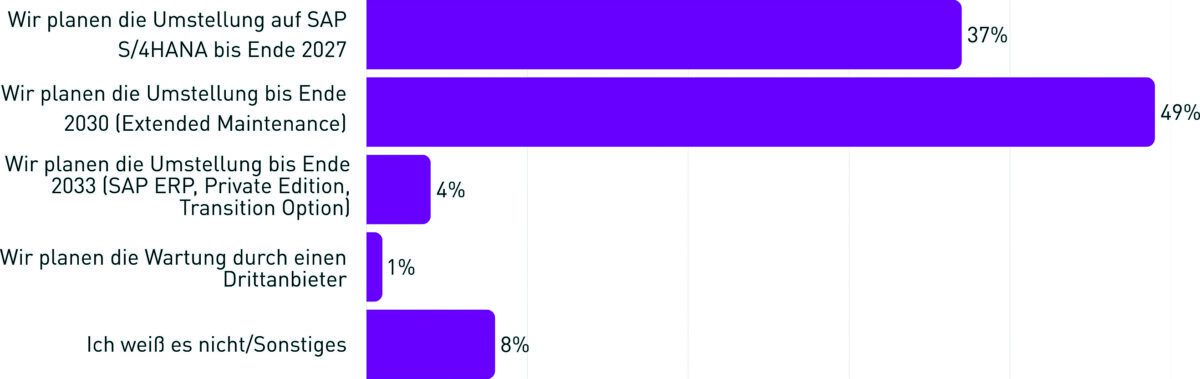

For the attentive observer of the SAP community, the figures in the latest DSAG Investment Report 2026 reveal a profound rift between SAP's glossy visions and the reality of existing customers. „The fact that some companies are not planning to switch to S/4 Hana until 2030 does not mean that they are waiting until then to make the switch. Rather, they simply need this time due to the complexity of their system landscapes. I see this as an expression of the reality in IT departments. A shortage of skilled workers, parallel transformation projects and limited budgets are also leading to schedules being pushed back - even if this results in higher maintenance costs,“ says DSAG boss Jens Hungershausen.

Forced paradigm shift

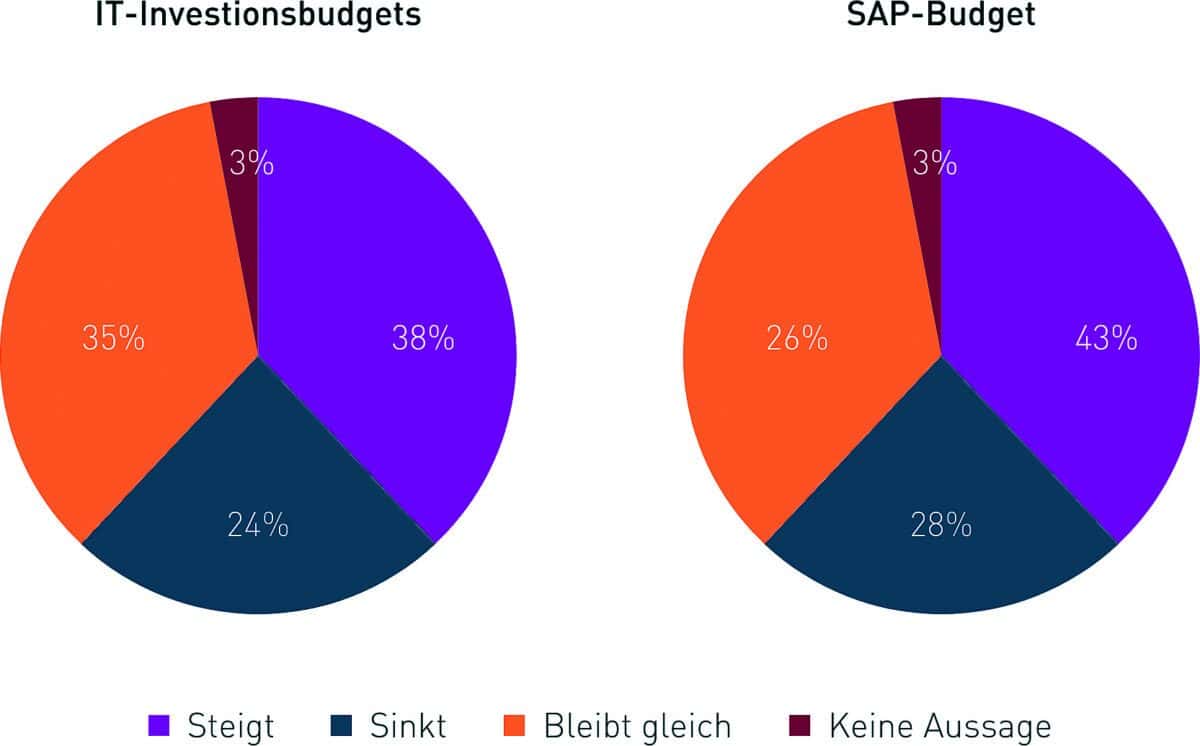

While SAP CEO Christian Klein and CFO Dominik Asam were at times able to celebrate historic all-time highs on the stock markets with consistent cloud and AI rhetoric, a detailed survey by the German-speaking SAP User Group (DSAG) shows that the forced paradigm shift is meeting with massive resistance and deep skepticism among existing customers. Budgets for IT and SAP continue to grow, but with the handbrake noticeably applied and under the strictest criteria of economic viability, because according to the report, general IT budgets are only increasing at 38% of the companies surveyed, while they remain the same at 35% and are even decreasing at 24%.

An identical picture emerges for pure SAP investments, which are only growing at 43% of DACH companies, while 28% are now reducing their expenditure in the SAP environment. This financial restraint is not a sign of technical disinterest, but rather the result of deep uncertainty in the face of geopolitical tensions, high energy prices and, above all, an extremely complex and sometimes customer-hostile license and contract structure on the part of SAP.

License models as a stress test

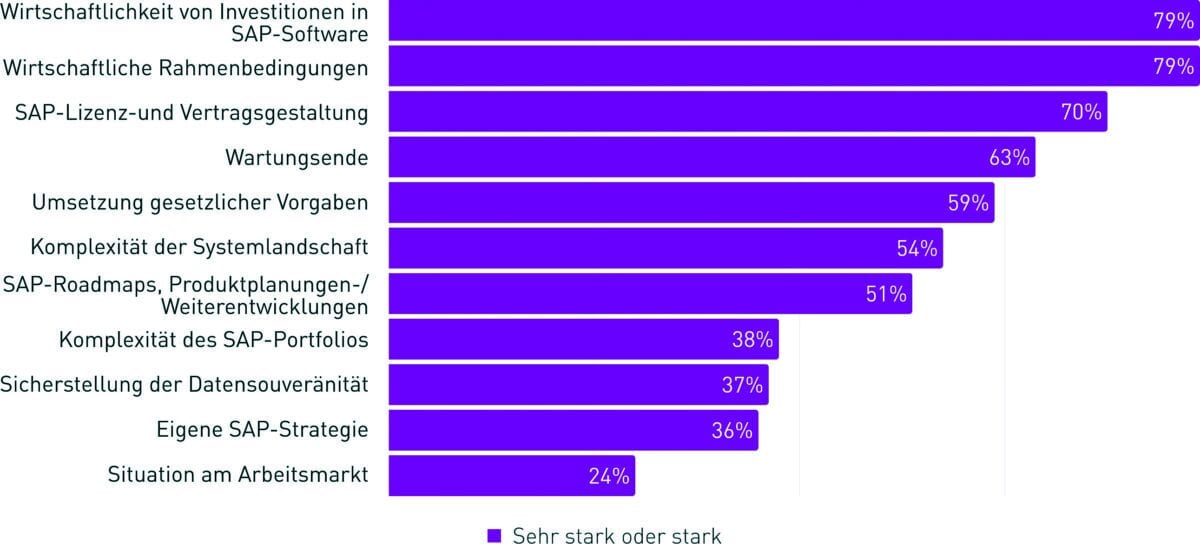

When 79 percent of DSAG members name the profitability of investments in SAP software and the general economic conditions as the greatest challenges and 70 percent openly complain about the SAP license and contract structure, then this is like an oath of disclosure for the Walldorf partner management. Although SAP's strategic relevance remains formally intact, with 48% of customers rating the provider's importance as unchanged and 36% as increasing, this status quo is less the result of genuine technical enthusiasm than of the historical penetration of core processes, which makes a short-term exit virtually impossible.

The central battleground in this strategic battle between SAP and its existing customers is the ERP operating model of the future, with SAP leadership aggressively pushing customers into a subscription-based cloud infrastructure with programs such as Rise with SAP and Grow with SAP.

Marginal phenomenon of the public cloud

However, the reality in the data centers of the DACH region, as well as internationally in the USA, UK and Japan, belies these cloud-only dreams. The joint survey by the international user associations ASUG, DSAG, UKISUG and JSUG irrefutably proves that hybrid system landscapes form the undisputed backbone of the global economy.

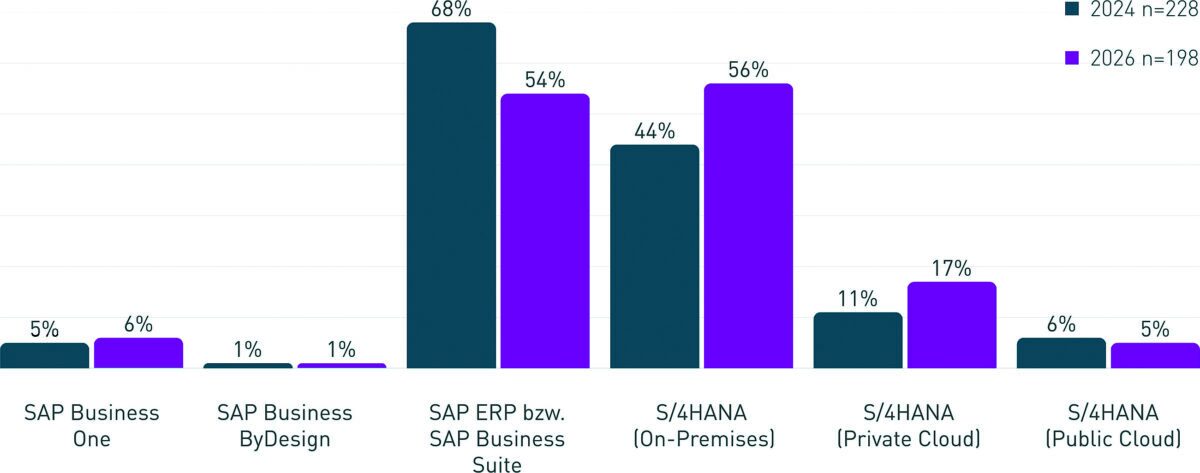

A staggering 78 percent of DSAG members currently operate a hybrid mix of on-prem and cloud solutions. In the complex ERP environment of existing customers, SAP's much-anticipated switch to the public cloud is a purely marginal phenomenon, accounting for a marginal percentage of DSAG members in operational terms and not even exceeding seven percent in future planning. Instead, 55 percent of German-speaking users continue to rely on S/4 Hana in classic on-prem operation, and on-prem also leads the planned new implementations with 31 percent, ahead of the private cloud edition with 35 percent.

Critical existing SAP customers often do not see models such as Rise with SAP as a technical or economic liberation, but rather as a strategic constraint for their organizational and operational structure that leads to an unprecedented vendor lock-in. Those who get involved with Rise give up their valuable, permanent on-prem licenses and enter into a non-transparent subscription model based on the full-use equivalent (FUE) metric, in which the long-term total cost of ownership (TCO) often rises uncontrollably and a sovereign cloud exit strategy is de facto not contractually provided for.

Although 40 percent of customers are trying to make the new SAP incentive program „Rise with SAP Migration and Modernization“ somewhat relevant, the fear of losing the system adaptations they have developed (63 percent) and deep data protection concerns about US hyperscalers (45 percent) mean that scepticism about a complete loss of control to SAP continues to dominate.

EU Data Act: a toothless tiger

The political promises from Brussels sound like a redemptive fanfare for long-suffering CIOs, as the EU Data Act explicitly acts as a regulatory corrective to break up the dreaded vendor lock-in and legally secure the change of cloud service providers or even a complete cloud exit.

The law obliges cloud providers to remove contractual and technical hurdles in order to ensure data portability and stipulates that so-called switching charges will be gradually reduced and completely banned from January 2027.

However, a closer look at the SAP architecture and the specific license mechanics of Rise quickly reveals this legal promise of salvation to be a treacherous illusion for existing SAP customers.

The technical reality lags miles behind the noble legal ambitions, because although the EU Data Act establishes a legal right to the release of data, it in no way solves the fundamental licensing problem of the lack of application logic after the end of a contract. If a user company leaves the SAP cloud, the EU law forces SAP to make the data removal technically and financially possible, but this says absolutely nothing about how the company can still use this data in a commercially viable way afterwards. The data „liberated“ by the Data Act is therefore a dead treasure that the company would have to make massive investments in external IT platforms to revive in order to put the raw tables back into a readable business context.

(multiple answers possible)

Target image of the new Business Suite

A new aspect of the DSAG Investment Report was the question of how strongly companies base their investment planning on the SAP target image of the „new“ SAP Business Suite (Cloud ERP, SAP Business AI, SAP Business Data Cloud and Business Technology Platform). 35% of respondents said they do this, while 62% said they are less oriented towards this. Four percent did not provide any information. „The picture is similar for both the Integrated Toolchain and the target vision of the new SAP Business Suite: companies expect clear statements on added value, integration into existing landscapes and economic viability. Only then will strategic target images be translated more strongly into real investment decisions,“ says Jens Hungershausen. And he adds: „If you consider that comparatively new products such as Business AI and the Business Data Cloud are already part of the target vision for a good third of respondents, this is a positive message.“

Clean Core: an invasive procedure

To enforce this architectural and commercial transformation, SAP has proclaimed the concept of Clean Core as the overriding development doctrine, which is akin to radical and painful open-heart surgery for existing SAP customers. The Clean Core strategy is relentlessly aimed at transforming the digital core of

To completely free SAP S/4 Hana from historically grown, customer-specific Z programming and Abap modifications in order to keep the software standardized, low-maintenance and, above all, smoothly releasable in the future.

SAP has established a strict four-level classification model for this, which ranges from Level A, the upgrade-stable APIs explicitly released by SAP, to the Business Technology Platform or Abap Cloud, right through to the frowned-upon Level D, in which classic and insecure modifications to the SAP standard code are severely penalized.

(multiple answers possible)

Strategic BTP bottle neck

For decades-old SAP customers whose competitive advantages are deeply rooted in the modified ERP core, this clean-core constraint means an extremely resource-intensive archaeological excavation in which millions of lines of old code have to be analyzed, sorted out and completely redeveloped. SAP is thus rigorously shifting the effort of individualization to the outside, which inevitably leads to the secret star and at the same time the biggest strategic bottleneck of the current SAP architecture: the Business Technology Platform.

BTP without alternatives

BTP is the technical foundation without any alternative to be able to map company-specific extensions, integrations and AI scenarios in a clean-core world. Consequently, BTP is the undisputed leader of all strategic Software-as-a-Service solutions in the DSAG Investment Report 2026, accounting for 39% of high and medium investments.

Customers primarily use BTP for complex integration tasks (45%) and data-driven analysis solutions (38%) in order to somehow hold their fragmented hybrid landscapes together. However, detailed observations show that BTP is far from a smooth panacea in practice. The SAP community massively criticizes the completely non-transparent, consumption-based payment models such as the Cloud Platform Enterprise Agreement (CPEA) or the new BTP Enterprise Agreement (BTPEA), where pre-purchased credits can expire at the end of the year, which puts IT managers under massive commercial pressure. DSAG also criticizes the inconsistent architecture within BTP itself, the lack of consistent identity management

strategies and poor usability across the numerous purchased microservices.

Steampunk versus freedom

Although SAP now also offers BTP on the infrastructures of all major hyperscalers such as AWS, Microsoft Azure and Google Cloud, many developers feel that the strict requirements of the Abap Cloud - known internally as Steampunk - severely restrict their architectural freedom. Steampunk prohibits direct access to database tables or traditional file systems and instead enforces the exclusive use of approved SAP APIs or modern frameworks such as the Cloud Application Programming Model (CAP) and the RESTful Application Programming Model (RAP).

Reinventing architecture

For existing SAP customers, this means that they not only have to completely reinvent their software architecture, but also retrain their entire development team in a lengthy process to a completely new, cloud-native paradigm, which is an almost impossible task given the chronic shortage of skilled workers in the SAP Basis. SAP's strategic vacuum is even more dramatic in the area of data management, where the Group is now trying to regain lost ground with the new Business Data Cloud (SAP BDC) following the resounding failure of the resource-guzzling SAP Data Hub. The BDC, the technical heart of which is the SAP Datasphere virtualization platform, is intended to solve the fundamental problem of fragmented data silos by acting as a business data fabric. Instead of physically and cost-intensively copying and moving data (ETL processes) as in traditional data warehouses, the data should remain in its original location thanks to the BDC and merely be linked semantically. However, the critical analyst immediately recognizes in the BDC the bitter admission by Walldorf that it has long since lost touch in the area of big data and advanced analytics. To counteract the migration of customers to generic cloud platforms, SAP has had to enter into far-reaching and deep partnerships with former rivals such as Databricks and Snowflake.

Databricks and Snowflake

Using technical bridges such as „zero-copy connectivity via delta sharing“, SAP now allows Databricks and Snowflake AI algorithms direct, redundancy-free access to semantically enriched SAP core data. What SAP is celebrating as a major step towards an open data ecosystem is actually revealing an impending loss of sovereignty: SAP is increasingly degrading itself to a pure, interchangeable data supplier for the superior AI and machine learning engines of US hyperscalers and data specialists.

Moreover, existing SAP customers do not seem to understand or accept this complex BDC strategy at all. The DSAG Report 2026 reveals that 31 percent of users are not familiar with the Business Data Cloud at all and only 15 percent describe themselves as really familiar with the solution. There is a massive lack of information about integration capability, contractual hurdles and the actual differentiation from old business warehouse structures, which is why the user association is quite rightly calling vehemently for more transparency and educational work by SAP. This blatant failure of communication and strategy ultimately culminates in SAP's current artificial intelligence policy, which is increasingly perceived by customers as extortionate and hostile to innovation. In the frenzy of generative AI, SAP CEO Christian Klein announced the fatal decision in the summer of 2023 to make essential AI innovations, the digital assistant Joule and sustainability solutions such as the Green Ledger available exclusively to those customers who can be forced into the expensive cloud subscriptions of Rise or Grow.

The downside of the AI boom

For the base of on-prem customers who rely on S/4 Hana in their own or hosted data centers and have invested millions in their systems in some cases, this embargo is like a massive breach of trust and a paradigm shift. SAP is clearly not using AI here primarily to solve complex business problems, but is abusing the hype as a commercial thumbscrew for its stagnating public cloud transformation. The market relentlessly delivers the receipt for this policy in the DSAG Report 2026: Although 45 percent of users consider AI to be highly relevant for future investments, when AI is already being used productively today, 77 percent of customers fall back on non-SAP solutions from OpenAI, Anthropic, Microsoft or Aleph Alpha. Customers are fleeing the complex, expensive and restrictive SAP AI cosmos and building their own intelligence around the ERP system. „These figures should be seen in the context of the basis of the survey and the varying complexity of application scenarios. Different requirements apply for a use case in the SAP environment than for the use of standard solutions based on large language models, for example,“ says Jens Hungershausen.

“The reality check shows that the use of AI in business processes is still rather difficult. The fact that use cases predominantly involve non-SAP

solutions are implemented is a signal to SAP.”

Jens Hungershausen,

Chairman of the DSAG

A deeply integrated, context-sensitive AI strategy, as outlined by SAP with its Agentic AI vision, would be revolutionary for corporate management. Agentic AI goes far beyond simple chatbots; it involves autonomous AI agents that are capable of independently orchestrating and executing end-to-end processes such as procurement, supply chain management or financial transactions across system boundaries. However, the SAP community views these autonomous agents with technical skepticism. An autonomous Joule agent that independently triggers orders or changes bookings in the private cloud requires an absolute maximum of system stability, deterministic predictability and, above all, excellent, error-free master data quality - prerequisites that are simply not available in the historically grown, often poorly maintained data landscapes of many existing customers.

AI agents out of control?

Who controls the AI agent if it makes incorrect supply chain decisions due to a hallucination in the hyperscalers„ linked language models? The legal and operational risks are immense, and until SAP clarifies these elementary governance and liability issues, experts warn of an unmanageable “Frankenstein architecture„ (quote from SAP Executive Board member Thomas Saueressig) in which AI agents from Salesforce, Workday and SAP collide with each other in an unregulated patchwork quilt. “The reality check also shows that the use of AI in business processes is still rather difficult. The fact that corresponding use cases are predominantly implemented with non-SAP solutions is also a signal to SAP. Many companies are still working with on-prem systems or highly individualized landscapes in which AI innovations can only be used to a limited extent. As a user association, we would like to see more freedom of choice, transparency and realistic migration paths," says DSAG CEO Jens Hungershausen.

Conclusion: 2026 as a turning point

In summary, the detailed analysis of the DSAG Investment Report 2026, the ASUG figures and current market developments shows that 2026 marks a historic turning point for existing SAP customers. SAP's attempt to force its loyal customer base into a standardized, AI-driven public cloud with a crowbar has effectively failed in Europe. Customers are defending themselves against the threat of vendor lock-in, ignoring the public cloud and defending their digital sovereignty by consciously building hybrid, composable IT landscapes (composable ERP). Existing SAP customers are using independent integration platforms such as Boomi, data lakehouses from Databricks and generic hyperscaler AI to free themselves from the technical, business, organizational and licensing constraints of the Walldorf-based company.

SAP remains the indispensable transactional heart of the company, but its monopoly on real innovation is rapidly crumbling. If SAP does not quickly stop putting its own share price above the real technical and economic needs of its community, create transparent and fair licensing models for the on-prem and BTP world and unconditionally lift the AI embargo, the former ERP giant risks degenerating into a pure, high-priced database management software in the long term, while the actual entrepreneurial value creation has long been taking place on the agile platforms of the competition.

The DSAG report is an unmistakable wake-up call: SAP customers in 2026 are demanding clarity, freedom of choice, investment protection and a pragmatic technical discourse at eye level - and no elitist, stock market-driven cloud fairy tales from Walldorf.

Assessments of the key findings from Austria

Walter Schinnerer,

DSAG Board of Directors Austria

From DSAG's point of view, it is hardly surprising that many user companies continue to prefer on-premises for their S/4 Hana transformation - and predominantly opt for controlled private cloud models in the cloud. After all, cloud solutions cannot be implemented equally in all companies and industries. Regulatory guidelines and security requirements sometimes set strict limits here. In addition, it remains to be seen in practice to what extent sovereign cloud offerings actually meet the specific requirements.

The appeal to the software group is therefore once again: less pressure to migrate to the cloud, more focus on reliable framework conditions, functional depth and sustainable planning security. Transformation needs a sense of proportion. The same applies: innovations must not be reserved exclusively for the cloud, but must also be available to S/4 Hana on-premises customers with a comparable scope of services - in the interests of genuine freedom of choice and in the interests of users.

Assessments of the key findings from Switzerland

Markus Bierl,

DSAG Board of Directors Switzerland

In view of the ongoing tense global market situation, it is understandable that companies are scrutinizing their investments very closely. When asked how strongly certain challenges influence their SAP investment decisions, 79% of respondents cited both the economic conditions and the profitability of investments in SAP software. This sends a clear message to the software group: transformation projects mean high costs and resource expenditure. If SAP wants to lead customers to new solutions and into the cloud, the Group must create convincing incentives and offer rapid, tangible added value.

The responses to the „new“ SAP Business Suite also underline this picture: the majority of respondents have so far aligned their investment planning less closely or not at all with the new target image. In other words: SAP solutions yes - but not at any price and only if the benefits are clearly recognizable.